AI integration has become a fundamental part of digital transformation for companies in the insurance industry. That said, AI applications – and their benefits – have evolved over the past decade.

Pre-2020, insurers primarily leveraged AI to assess and service claims based on the data provided by policyholders.

But today’s AI era represents a shift toward AI-powered predictive analytics and personalization that use data from external sources and devices to provide custom pricing, match leads with best-fit advisors, and more.

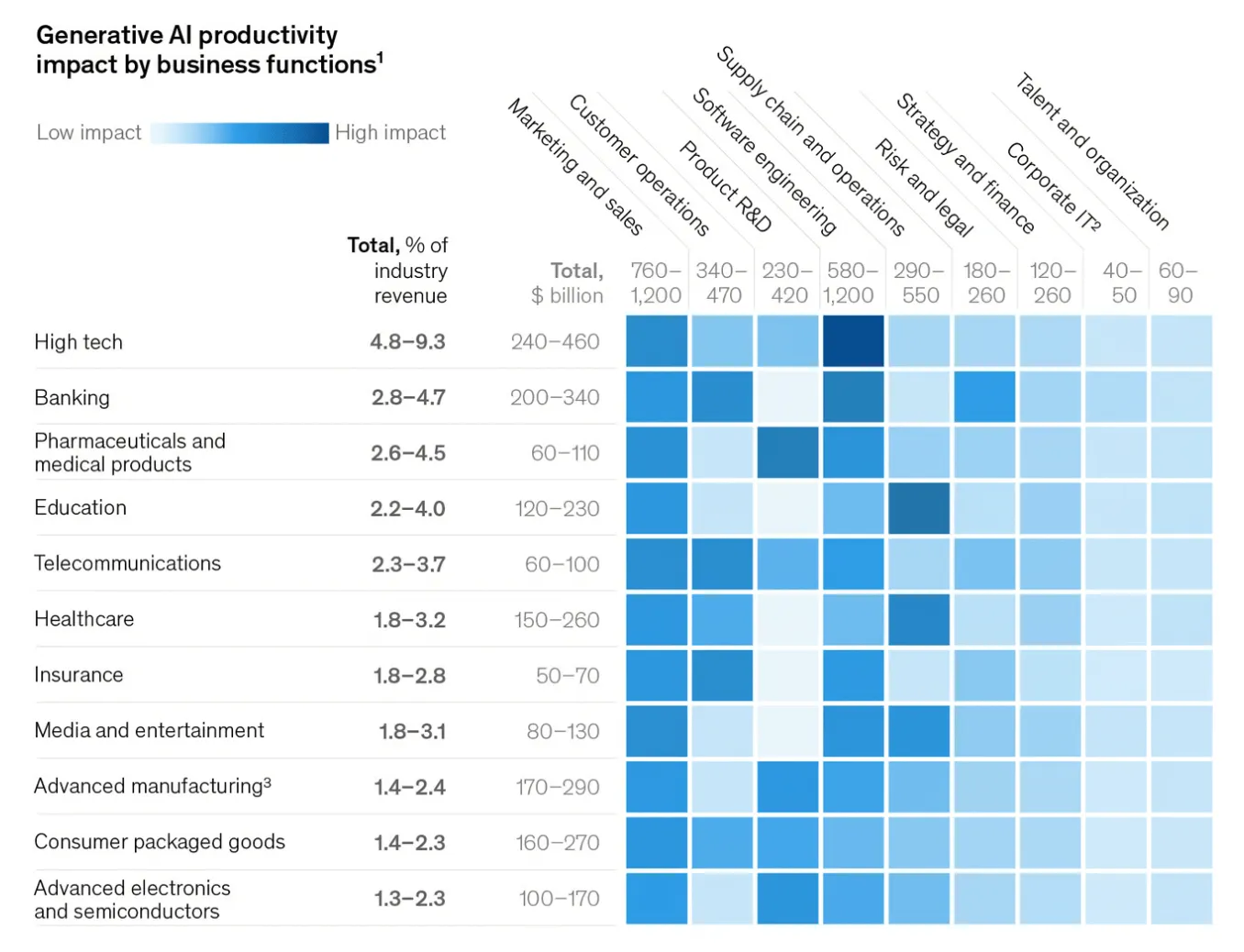

Insurers are also expanding their use of Generative AI solutions (GenAI), expected to generate $50 to $70 billion in revenue in this industry alone, with the highest impact predicted for marketing and sales, customer operations, and software engineering.

*Graph by Mckinsey & Company

This article will explore how AI can transform insurers’ operations, what challenges must be addressed before adopting AI, what the future holds for AI in insurance, and how to get started with AI integration.

3 Challenges in Adopting AI in Insurance

AI integration in insurance comes with substantial potential benefits, such as more accurate risk assessment and streamlined claim processing. However, these three challenges can pose a significant barrier to adoption if left unaddressed.

Regulatory Compliance

Insurance is an already heavily regulated industry on its own. In the United States, insurers must comply with federal laws (e.g., HIPAA for health insurers) and state legislation. Regulations span market conduct, capital and solvency, and consumer protection obligations, among others.

When it comes to AI, existing data protection and privacy laws already pose limits on how data for AI systems can be collected and processed. These laws include, most notably, the California Consumer Privacy Act (CCPA) and the EU General Data Protection Regulation (GDPR).

The ethics of AI use is already in the crosshairs of legislators in certain jurisdictions. The European Union is working on the AI Act, while NAIC members approved a Model Bulletin on AI use in insurance in late 2023. The latter focuses, among other things, on third-party data use in servicing insurance functions. Colorado may become one of the first states to regulate AI use in risk assessment for underwriting in the United States.

What this means for insurers: Any AI initiatives have to involve chief risk and compliance officers to properly identify legal constraints and put appropriate guardrails in place.

Legacy Burdens

The insurance industry innovation is driven by insurtech companies like Lemonade, Pie Insurance, and Hippo. The legacy burden is among the key reasons why some traditional insurers struggle to catch up with insurtech companies: their core application age averages 18 years.

Legacy technology, in turn, comes with several constraints that have to be addressed before implementing AI initiatives:

- Multiple disparate core platforms

- Ineffective data flows and data silos

- Lack of integration and difficulties in integration because of outdated technologies

- Inability to or difficulties in leveraging cloud technology

What this means for insurers: Before pondering AI initiatives, traditional insurers first have to address their legacy estate and ensure their digital maturity is sufficient for AI implementation.

Reliability and Transparency

Depending on the model training approach, initial data sets, and implementation methods, certain AI solutions may produce biased, inaccurate, or misleading results. There’s also the black-box problem: black-box AI systems don’t explain their results, and the exact way how the algorithms produced the output can be hard or impossible to pin down.

This can pose a significant risk for insurers using AI to automate processes like underwriting and claim settlement. For example, Cigna is currently dealing with a class action lawsuit filed for allegedly automatically denying patients’ claims without any review by a qualified physician.

What this means for insurers: The training sets have to be carefully put together to ensure only high-quality data is included in them. The AI system development and testing have to account for transparency, explainability, and auditability requirements.

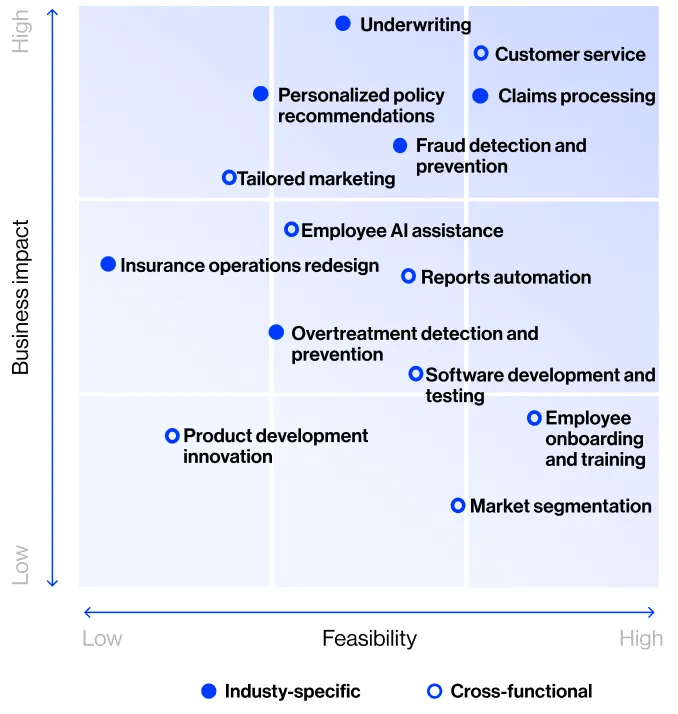

3 Top Use Cases for AI Integration in Insurance

Let’s break down three key use cases for AI in insurance: policy recommendations and marketing, claims management, and fraud detection and prevention.

Coverage Recommendations and Policy Marketing

AI systems can transform policy marketing by:

- Going beyond correlations to hyper-personalize coverage recommendations. Causal AI can pinpoint cause-and-effect relationships in user choices, increasing recommendation performance by up to 20%.

- Generating recommendations based on zero or few interactions. The GLLM4Rec approach overcomes data limitations in generating recommendations, making them twice as efficient at customer acquisition.

- Facilitating customer interactions with GenAI-powered natural dialogue. This improves user engagement as conversational AI can break down complex policies in simple terms. Explainable GenAI, in turn, can provide clear reasoning behind underwriting and claims decisions to foster trust.

Introducing AI in marketing can increase new policy sales and reduce churn by as much as 30%.

Claims Management

In claims management, enterprise AI solutions can streamline processes by enabling intelligent document processing. It can include:

- Automating claim triaging. Based on historical data, predictive analytics can determine the most suitable processors for each claim.

- Confirming coverage eligibility. AI solutions can automatically verify that the policyholder is eligible to submit a claim under their current coverage.

- Generating assessments. Large language models can process documents and customer interactions to produce claim reviews.

AI is already speeding up claim processing in insurance: Lemonade set the world record for the fastest claim settlement in 2016 with a three-second payout. (It also beat its own record in 2023 with a two-second claim settlement.)

Fraud Detection and Prevention

80% of insurers consider fighting fraud a priority – but keeping up with new forms of fraud remains the number one challenge, according to FRISS. AI can step up insurers’ fraud detection and prevention capabilities by enhancing fraud risk assessment.

Using hundreds of data points, AI solutions can identify fraudulent patterns and flag potentially fraudulent claims more accurately than a human possibly could.

Pre-trained LLMs that are fine-tuned on enterprise data are 5% more accurate at fraud and risk prediction than traditional ML solutions. At the same time, an explainability layer put over traditional ML solutions can act as a certified CISM security manager in most cases.

5 Examples of Insurance Companies Leveraging Enterprise AI Solutions

How do insurers leverage AI in a real-world setting? Here are five examples of AI used in claims processing, underwriting, parametric insurance automation, and more.

Treatline

Neurons Lab partnered up with Treatline, an innovative insurtech company, to deliver a prior authorization platform for health insurance. It leverages AI for intelligent document processing (powered by natural language processing, optical character recognition, and computer vision) and a GenAI criteria-matching system.

Treatline expects the platform to reduce peer-to-peer reviews by 30% and decrease the time spent on administration by 70%.

AXA

In July 2023, AXA made its own version of ChatGPT, dubbed AXA Secure GPT, available to its 1,000 employees. Meant to boost employee productivity, the platform was also designed with security, privacy, and regulatory compliance in mind.

The platform’s GenAI capabilities include generating, summarizing, correcting, and translating text and code, as well as working with images.

Swiss Reinsurance Company

This Swiss reinsurance company uses AI for predictive analytics-powered underwriting triaging in life and health insurance. An AI model is also the foundation for Swiss Re’s parametric Flight Delay Compensation insurance platform that can predict flight delays and adjust rates using machine learning and 200 million historical data points.

Zurich Insurance Group

Zurich Insurance Group has been using AI long before the GenAI hype: the company acquired an Estonia-based conversational AI company in late 2021 and currently has over 160 use cases for AI. One such use case involves AI-driven automation that speeds up personal injury claim processing to seconds instead of an hour.

ZhongAn

ZhongAn, a leading Chinese insurance company, leverages AI to increase the rate of enterprise data utilization, streamline underwriting, and automate claim processing. According to the company’s CEO, over 99% of ZhongAn’s claim processes are automated. The company also used AI to deploy smart interactive voice response that handles over 85% of customer queries.

The Future of AI in Insurance

The developments in AI technology are laying the groundwork for a fundamental industry-wide shift from “detect and repair” to “predict and prevent,” as McKinsey puts it. Instead of focusing on claims and payouts, insurers of tomorrow will leverage AI to help policyholders prevent the insured events altogether.

As the volumes of data generated, including data from connected devices, increase exponentially, AI systems can leverage more and more data points to produce more accurate results. The number of IoT devices alone is expected to almost double between 2023 and 2030 to 29.5 billion.

Here are the five future trends in insurance AI that are poised to shape the industry in the years to come:

- Preventative maintenance and early issue detection powered by IoT data (e.g., minimizing mold damage by monitoring humidity)

- Usage-based car insurance (e.g., pay-as-you-drive, pay-how-you-drive), which leverages AI to assess driving behaviors using connected vehicle data

- Accelerated sales cycles thanks to largely or fully automated risk assessment and underwriting that also complies with regulators’ push for traceability of the risk score

- Continuous underwriting based on real-time data that allows for recalculating risk profiles

- Computer vision-powered damage assessment solutions that automatically translate videos and photos of the damaged property into estimated repair costs and loss description

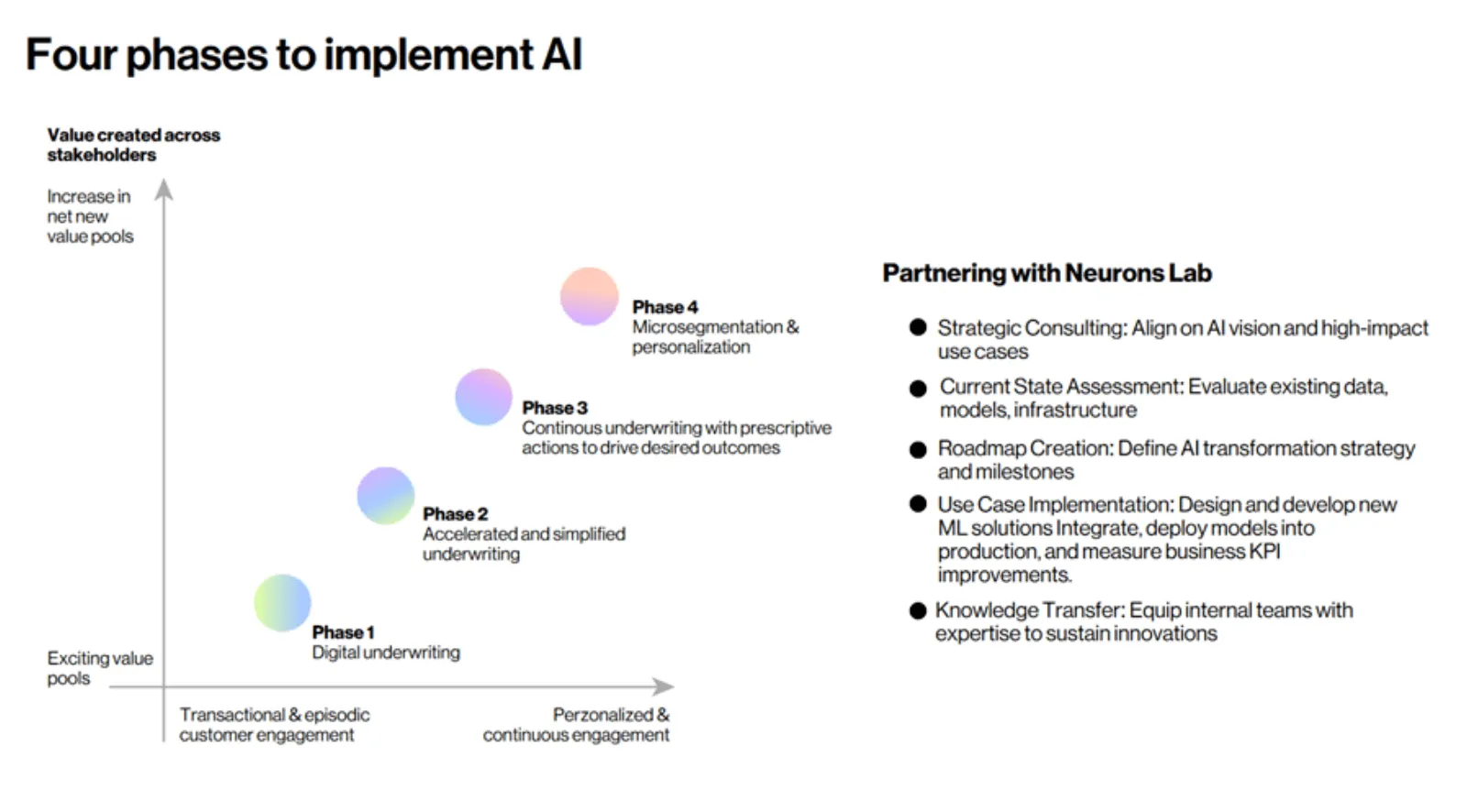

How to Get Started with AI Integration in Insurance

Leveraging AI in insurance operations is a four-phase journey that consists of implementing:

- Digital underwriting

- Accelerated and facilitated underwriting

- Continuous underwriting with prescriptive actions to drive preferred outcomes

- Microsegmentation and personalization

Each subsequent phase increases the value gains for stakeholders. It also drives the transformation from transactional and episodic customer interactions to highly personalized, continuous engagement.

As an AI consultancy for insurance, Neurons Lab offers end-to-end services in AI implementation. With 100+ completed AI projects and a talent pool of 500+ talented engineers, we have what it takes to:

- Identify the most impactful AI use cases and validate them with a proof-of-value

- Design, build, and deploy the AI system

- Scale your solution

Uncertain how exactly your organization can benefit from AI? Our AI Design Sprint will help you identify the most value-adding use cases and clarify the costs of leveraging AI.

The sprint involves feasibility and cost-benefit analysis, risk assessment and mitigation strategy, prototyping, and proof-of-value development and evaluation.

Frequently Asked Questions

What are the top use cases for AI in insurance?

The top use cases for AI integration in insurance include:

- Hyper-personalized coverage recommendations and policy marketing, as well as conversational AI interfaces

- Intelligent document processing in claims management to automate claim triaging, coverage eligibility verification, and assessment generation

- More accurate fraudulent pattern identification based on hundreds of data points for fraud detection and prevention

What are the challenges in implementing AI in insurance?

Implementing an AI system in insurance operations requires addressing the following challenges:

- Regulatory pressure, both from existing privacy (e.g., CCPA, GDPR) and industry-specific laws (e.g., HIPAA) and the regulations on AI use that are in the works in certain jurisdictions (the EU, Colorado)

- Legacy burdens that traditional insurers have to deal with to ensure data flows, integrations, and overall digital maturity are suitable for AI system implementation

- Reliability and transparency of AI systems’ output, ensuring which requires a careful approach to the training data sets, development, and testing

How do I get started with AI integration in my insurance organization?

We advise you to start by identifying the exact opportunities for AI implementation within your organization and prioritizing them based on the expected added value and costs. We also recommend you conduct a feasibility and risk analysis and develop and evaluate a proof-of-value before committing to a large-scale implementation.

We can help you do all of this with our AI Design Sprint. Our experts will help you zero in on the most impactful use cases and validate your solution with a proof-of-value.

About us: Neurons Lab

Neurons Lab delivers AI transformation services to guide enterprises into the new era of AI. Our approach covers the complete AI spectrum, combining leadership alignment with technology integration to deliver measurable outcomes.

As an AWS Advanced Partner and GenAI competency holder, we have successfully delivered tailored AI solutions to over 100 clients, including Fortune 500 companies and governmental organizations.