As a retail bank researching AI, you probably want to understand how it can deliver real business value. That’s because even though you may have already invested in AI tools like Microsoft Copilot or Anthropic Cowork,

- You’re seeing only modest productivity gains (often around 10%), even in areas where you expected significant improvement, like internal support, reporting, or simple customer queries

- You’ve hit a wall for multi-step workflows like KYC or onboarding that require more complex automations than your current tools can handle

- You’re unsure how to move beyond a simple back-office assistant and apply AI to more customer-facing processes, like support or cross-selling

As an AI exclusive enablement partner specializing in financial services, here at Neurons Lab we see this pattern of retail banks being stuck between experimentation and production often. But the challenge isn’t the AI tools you’re using. It’s not knowing how to apply them to real workflows that drive revenue and improve customer experience while reducing manual workloads.

Without addressing this, you risk falling behind competitors who are already using AI to process faster, serve customers better, and scale without adding headcount. In this article, we’ll break down where AI can deliver value in retail banking today, and how to move from isolated tools to systems that actually run even your most complex workflows.

In this article, we cover:

- AI’s Potential in Retail Banking: From Assistant to Autonomous Systems

- Top Use Cases for AI in Retail Banking

- How to Get Started with AI in Retail Banking

- How Neurons Lab Can Help You Implement AI for Retail Banking

- How a National Bank Achieved 85% Reduction in Document Processing Time with AI

- FAQs

Want to get started with implementing AI across key retail banking workflows? Get in touch with us today to get started.

AI’s Potential in Retail Banking: From Assistant to Autonomous Systems

As a retail bank using artificial intelligence solutions like Microsoft Copilot, ChatGPT, Anthropic Cowork, or similar tools, you’re likely using them for isolated tasks like Q&A over knowledge bases, email drafting, and internal chatbot-style interactions.

These tools act as virtual assistants. They respond to prompts, generate content, and support individual jobs to be done.

But, out of the box, they cannot execute workflows end-to-end independently. This means they can’t run in the background, move across your systems, or handle multi-step tasks. They’re also designed for internal use, so they can’t address customer-facing use cases.

As a result, your AI remains isolated from core operations. Teams still coordinate workflows manually, and complex jobs see little improvement.

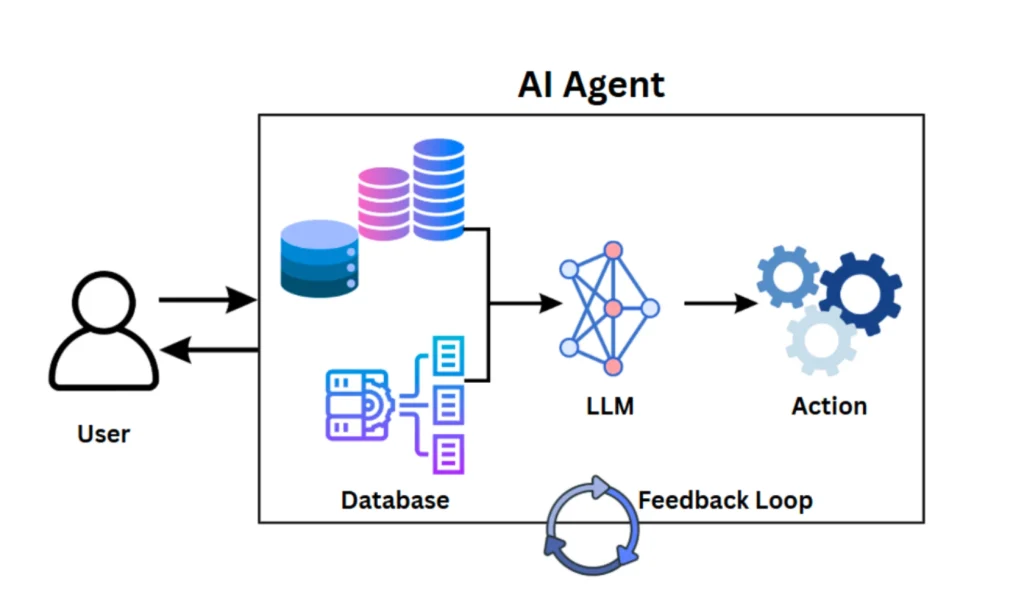

How Agentic AI Enables End-To-End Retail Banking Workflows

With Agentic AI, you can transition from chat-based interaction to task execution. AI agents can run processes in the background, access multiple data sets, and complete multi-step workflows with limited human input. Instead of generating answers, AI agents execute entire flows.

Let’s take onboarding as an example. Agents can move across systems like core banking data, CRMs, and external KYC/AML data providers. They can pull customer-submitted documents (e.g., IDs, income statements), cross-check them against transaction history or credit bureau data, and validate everything against compliance rules before moving the application forward without manual coordination.

This changes how AI fits into your operating model. Rather than limiting its support to single tasks, it becomes part of the workflow itself, handling multiple steps across various processes and teams.

But this step up in capability can’t be handled by a single AI model or tool. It requires the orchestration of multiple components, including data access, system integrations, and the logic defining how to execute tasks.

Why This Matters For Retail Banks

With agentic AI, processes that previously required handoffs between front office, compliance, and operations, and coordination across core banking systems, CRM, and KYC/AML tools, can now run end-to-end within a single flow.

This reduces the need for human coordination. You no longer need to manually pass tasks between systems and departments because workflows progress automatically, step by step.

Execution speed increases as a result.This means processes like customer application handling can run faster and at higher volumes without adding headcount.

This is where AI starts to deliver measurable outcomes across core operations, rather than a tool layered on top of your workflows that give you incremental gains in one-off tasks.

For a deeper look at how agentic AI is shaping banking as a whole, explore our full guide: Agentic AI in Banking: All You Need to Know

From resolving customer requests faster to processing account applications from start to finish, this potential spans both front and back office use cases that previously required multiple tools, systems, teams, and manual steps.

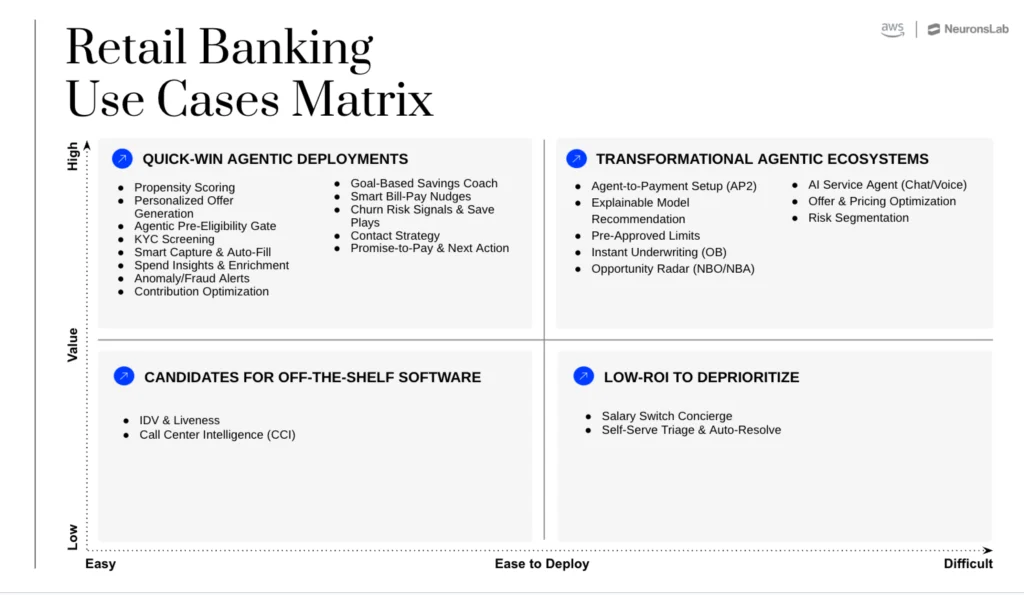

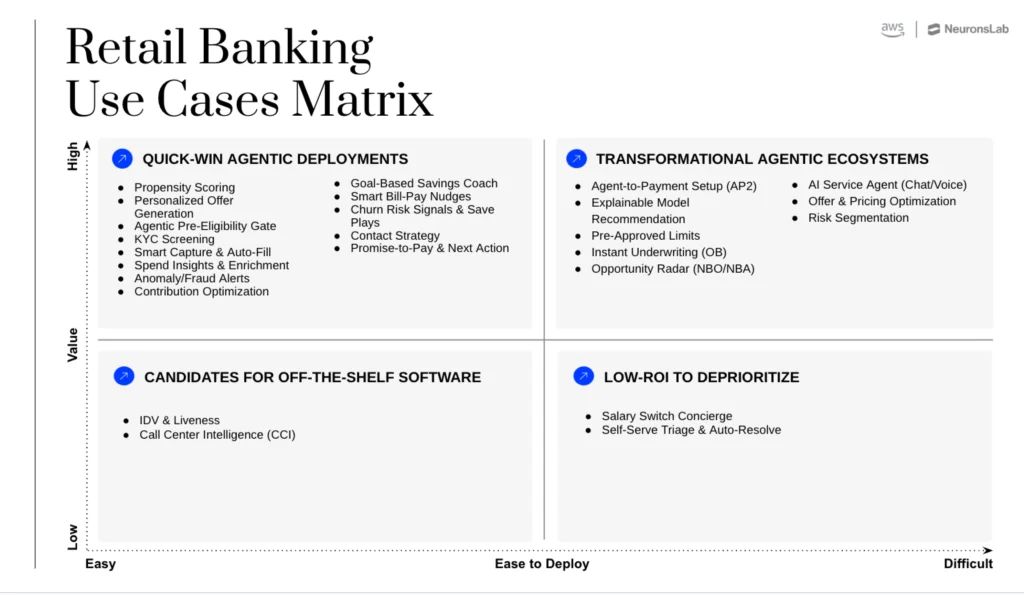

Top Use Cases for AI in Retail Banking

In retail banking, AI can support the entire customer journey, from onboarding and servicing to lending, collections, and long-term customer growth.

Use cases typically fall into two main groups: back office applications that reduce manual work and increase efficiency, and front office applications that improve customer experience and drive revenue. It also includes hybrid use cases that cover both front and back office.

Retail Banking Back office: AI-Powered Document Processing, Compliance, Lending, Collections and Engineering

AI supports back office teams across various key processes:

1. Help engineering teams build, maintain, and ship faster

With AI, engineering teams can build and maintain systems faster, reducing bottlenecks across development. Since engineering is one of the most expensive functions in retail banks, this allows teams to keep development costs more predictable as output increases.

2. Speed up KYC and onboarding document verification

Operations teams have to manually review and verify multiple documents for know your customer (KYC) and anti-money laundering (AML) checks before a customer’s loan or account application can move forward. But this is time consuming and slows onboarding.

AI agents can handle this process. They can classify incoming submissions, extract the relevant information, cross-reference it against KYC/AML requirements, and flag any missing or inconsistent data. Based on this, they can update internal systems and either move the application forward or escalate it for human review.

This reduces manual effort and allows teams to process applications faster, without increasing headcount.

3. Process legal documents and contracts across languages and jurisdictions

Self-employed customers and contractors who work with foreign companies often need to submit contracts in different languages.

AI agents can translate, extract the relevant details, and verify them against legal requirements. They can also flag inconsistencies or jurisdiction-specific risks for human oversight in your compliance team, making risk management more efficient.

This shortens review times, improves accuracy, and helps compliance teams scale the number of cases they can handle.

4. Verify transaction legitimacy and proof of funds

When customers run commercial transactions through their personal accounts or receive income from multiple countries, banks need to verify this activity.

AI agents can detect these transactions, flag them for review, analyze supporting documentation, and validate them against compliance rules and support fraud detection workflows. This significantly reduces investigation delays and frees compliance teams from routine checks.

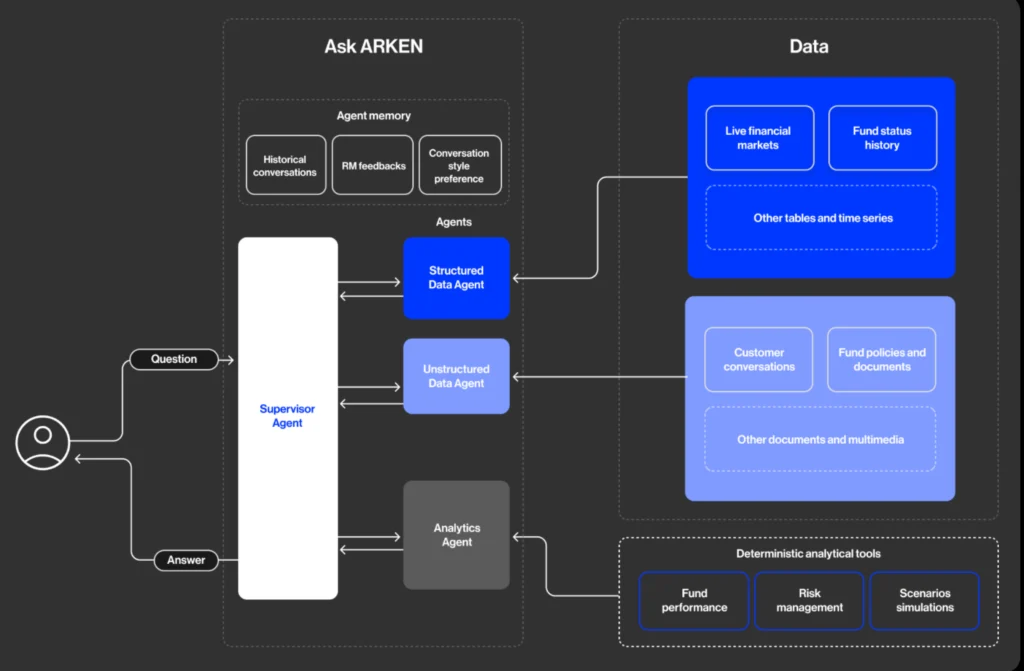

For example, one bank used ARKEN, Neurons Lab’s custom agentic AI system, to unify data across multiple legacy systems and automate compliance checks. As a result, relationship managers increased capacity, doubled client outreach, and improved net promoter score (NPS) by 15% through faster, more consistent customer engagement.

By reducing repetitive work across these back office functions, retail banks can get higher output without increasing team sizes.

Hybrid Use Case: Collections And Recovery

Collections is a multi-step process that spans both back-office systems and customer-facing interactions. It requires assessing risk, selecting the right actions, and engaging with customers to recover funds.

AI agents can coordinate these steps while maintaining control and auditability:

- On the back-office side, agents can analyze customer data, determine the appropriate recovery strategy, and execute outreach through channels like phone or messaging, while following compliance rules and maintaining full auditability.

- On the customer side, AI can handle conversations in real time. Instead of scripted, one-way calls, customers can ask questions, respond to AI-driven questions, and negotiate, while the AI agent adjusts its approach based on context and tone.

This creates a continuous workflow, where internal decisions and customer interactions are connected rather than handled by separate systems and teams.

For example, Neurons Lab did exactly this for a bank in Thailand. By replacing scripted robotic calls with AI-led conversations, the bank’s chances of recovering debt have increased significantly.

Front Office: Customer Experience, Personalization, and Revenue Growth

AI technologies support customer-facing teams across service, personalization, and new revenue opportunities:

1. Handle end-to-end requests across voice and chat channels

AI agents can manage customer requests from start to finish across both voice and chat. Instead of responding with information, they can execute tasks like processing transfers, issuing credit cards, or updating account details.

These requests often involve multiple steps and systems. For example, a simple request like “I lost my card” may require:

- Checking customer identity in the CRM

- Verifying recent transactions in the core banking system

- Blocking the card in the card management system

- Issuing a replacement through a separate processing service

AI agents can move across these systems, complete each step, and return a result to the customer within a single interaction.

This reduces the need for handoffs between customer support agents, operations teams, and back-office functions, as well as across channels like call centers, mobile apps, and chat.

With AI agents, retail banking customers receive faster resolution and support teams can handle higher volumes without increasing headcount.

2. Personalize Customer Experiences to Drive Engagement

Retail banks often rely on segmentation models to decide which products to offer, when to engage customers, and how to price or position those offers. These models typically group customers by broad attributes like income brackets or age, which don’t always reflect individual customer behavior.

This means banks miss signals like spending patterns, salary changes, product usage, or life events, which are more accurate indicators of what a customer actually needs.

This leads to poorly timed or irrelevant offers that don’t align with real customer needs, causing acceptance and engagement rates to drop.

With agentic AI, you can deliver tailored communication and recommend relevant products by analyzing each customer’s transaction history, income patterns, and product usage in real time. A customer whose income has grown consistently over two quarters might receive an offer to upgrade their account or have their loan limits adjusted automatically.

This leads to higher cross-sell conversion rates and stronger customer relationships

When Visa needed to deliver personalized marketing communications across markets, Neurons Lab built a generative AI (GenAI) and LLM-powered system with built-in compliance checks. This enabled Visa to generate tailored, channel-ready content in 20+ languages based on customer behavior and regional requirements. Read the full case study on How Visa Empowers its Marketing Teams with AI.

3. Send the right marketing messages at the right time to improve conversion rates

Even when banks identify the right offer, getting customers to actually act on it remains a challenge.

You might be scheduling campaigns in batches, sending them at fixed times, and pushing them through a limited set of channels, with little ability to adapt to what a customer is doing at that moment.

This means a customer might receive a loan offer after they’ve already secured financing elsewhere, or a savings product promotion when their account balance is low. These messages miss the moment when the customer is most likely to act.

AI agents can manage this marketing layer. They can generate and deliver messages based on signals like recent transactions, salary deposits, changes in account balance, product usage, and channel preferences.

For example, a customer who has just received a salary increase and maintains a higher average balance might receive an upgrade offer through their preferred channel, such as push notification or in-app message, at the moment those changes occur.

This improves engagement and conversion by aligning the offer with when the customer is most receptive and with how they prefer to engage.

4. Drive loyalty and retention through financial health guidance

AI agents can act as a personal finance assistant, continuously monitoring spending patterns, tracking progress toward savings goals, and triggering proactive nudges or product recommendations based on customer behaviour signals, such as an increase in monthly salary deposits.

For example, if a customer’s spending on dining or subscriptions increases over time, the agent can flag the trend, suggest a budget adjustment, or recommend a card with better cashback. If savings grow consistently after salary deposits, AI can prompt the next step, such as increasing savings targets or moving funds into an investment product.

Additionally, AI-driven guidance adjusts based on how the customer responds, getting more relevant over time. This creates an ongoing, tailored experience that helps customers make better financial decisions while strengthening long-term loyalty.

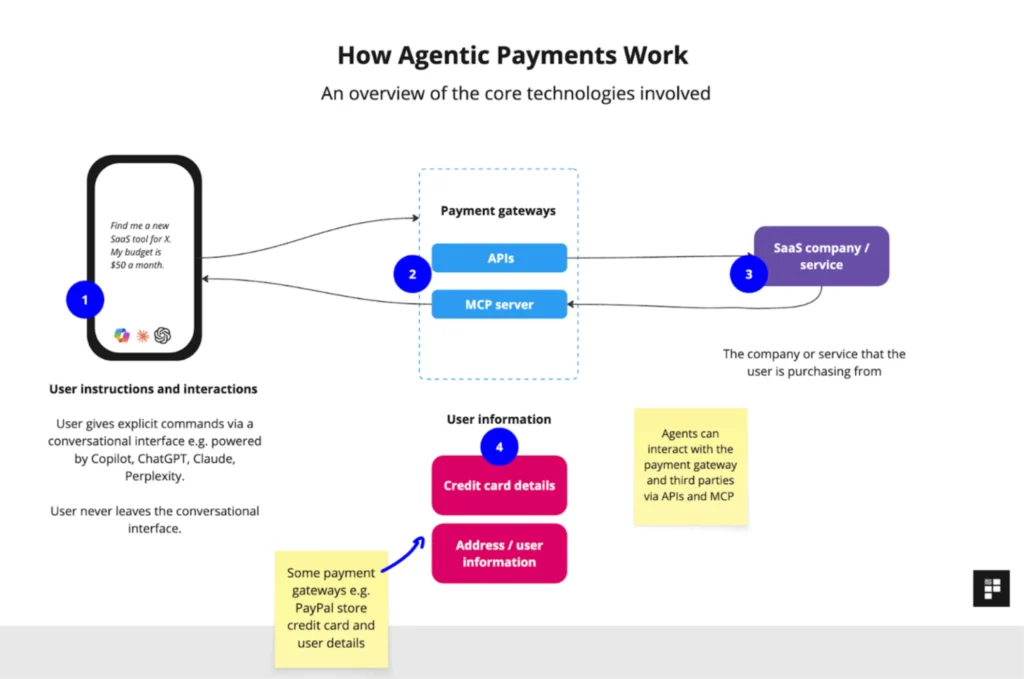

5. Create a new customer experience layer with agentic payments

While still in the early stages, agentic payments introduce a new interaction model where AI agents act as a bridge between the customer, the merchant, and the bank.

Instead of completing transactions through a banking app, customers are turning to agentic payments. They use AI assistants, such as ChatGPT or similar platforms, as virtual shoppers that can compare options and make purchases based on predefined budgets and personal preferences.

For example, the agent researches options for a round-trip flight, initiates a purchase, and request payment, while the bank authorizes and executes the transaction through its existing payment rails, such as account-to-account transfers or card payments.

This shifts the bank’s role from interface provider to transaction enabler. While it reduces direct interaction with banking apps, it increases the volume of transactions processed through the bank.

As customer shopping habits move toward AI-driven interfaces, banks that enable this model by offering their own agentic commerce solution can capture more activity, while those that don’t risk being bypassed entirely.

What It Takes To Run AI Agents In Retail Banking

Across these use cases, AI-powered agents allow retail banks to run processes faster, respond to customer needs in real time, and compete more effectively with fintechs on speed and experience.

To make this work, the same building blocks show up across every deployment:

- Agents need access to the right data, such as customer profiles, transactions, and product information

- Agents need to connect securely to core systems like CRM, core banking platforms, and payment infrastructure

- Workflows need to be clearly defined, so tasks can move between agents and systems without manual intervention

Getting these foundations right is what separates a working deployment from a proof of concept. That brings us to what implementing AI in retail banking looks like in practice.

How to Get Started with AI in Retail Banking

Many retail banks are already experimenting with AI initiatives in some form, but this alone rarely translates into faster processes or measurable gains in productivity. The gap between running a pilot and deploying AI that actually changes how your bank operates comes down to how you build, and we cover that below:

1. Start with Education

The lowest-hanging fruit is learning how to use the AI tools you already have in place, like Copilot or GPT.

Today, many teams use these tools as chatbots for tasks like drafting emails or answering questions. That delivers limited gains. AI literacy means understanding how to move beyond prompts and start thinking in terms of agents that can execute tasks across systems.

This baseline matters especially for back-office teams handling repetitive, manual work. Once teams understand how AI can move from answering questions to taking action, it becomes easier to identify where agents can replace or streamline entire workflows.

2. Prepare Data Access and Build the Right Architecture

Running agents effectively requires the ability to retrieve and act on data. This means you need to give agents:

- Access to data sources

- Tools that act on that data

- Skills, which are the logic that defines how those tools are used

That means you will need to prepare APIs and data endpoints covering the systems your agents will work across, such as account data, transactions, and debts. Without this, agents can’t operate.

Before exposing this data to agents, it also needs to be prepared. In many banks, data is fragmented across systems, duplicated, or inconsistently structured. This means cleaning and standardizing customer records, removing duplicates, and aligning data formats across systems so agents can reliably retrieve and act on it.

A collections agent, for example, needs to access a customer’s debt data during a call. If that access isn’t in place and data isn’t prepared, the agent can’t check or accurately convey what a customer actually owes in real time.

Agents operate by combining these elements into workflows, but this requires more than just access to data. You need tools that can take action within your systems, such as updating customer records, blocking cards, initiating payments, or triggering compliance checks. You also need skills, which define how those tools are used in practice, including business rules, decision-making logic, and how to handle edge cases.

This is what allows you to move from simple prompts to systems that can execute tasks end to end. It’s not something standalone tools can achieve on their own.

3. Move From Simple Use of AI To Custom Agent Development

To move from simple AI to production systems, keep these key considerations in mind:

- Understand the limits of your current tools. Most copilots and AI assistants are designed for chat-based tasks like answering simple questions. They cannot access your systems or execute actions across workflows. Advanced use cases like collections or payments require agents that can operate across multiple systems, apply business rules, and complete multi-step processes end to end.

- Set up strong governance for data access. AI needs real-time access to internal data to be useful, but that access must be controlled through clear permissions, auditability, and compliance guardrails. If this isn’t set up correctly, you either over-restrict access and block important workflows, or expose data in ways that create risk.

- Prepare for AI-led customer interfaces. Customers are already interacting with banks through AI assistants. To support this, your core systems need to be accessible via APIs, so agents can retrieve data and execute actions directly within your systems, without relying solely on your existing apps or support channels.

4. Keep your Approach Simple

The development model for retail banks is straightforward:

- Build AI literacy

- Prepare your data and systems

- Build agents that execute workflows

While the steps are simple, execution isn’t. Connecting systems, exposing data securely, and designing agent workflows requires engineering and domain expertise that most internal teams don’t have in place today.

This is where many banks get stuck, unable to move from pilots to production, and where specialized expertise becomes critical.

How Neurons Lab Can Help You Implement AI for Retail Banking

At Neurons Lab, we specialize in taking retail banks from pilot to production. With us, you can implement systems that handle core retail banking processes like onboarding, support, lending, and collections, delivering measurable outcomes across speed, productivity, and system integration.

Based in the UK and Singapore, we’re an agentic AI consulting firm serving financial institutions across North America, Europe, and Asia. As an AI enablement partner, we design, build, and implement agentic AI solutions tailored for mid-to-large BFSIs operating in highly regulated environments, including banks, insurers, and wealth management firms.

Trusted by 100+ clients, such as HSBC, Visa, and AXA, we co-create agentic systems that run in production and scale across your organization.

With our tailored AI strategy consulting and agentic AI development for retail banking, you’ll be able to:

Build AI Literacy That Translates Into Execution

If your teams are only using AI for repetitive tasks like drafting emails and answering questions, you’re unlikely to see meaningful improvements in productivity. With Neurons Lab, both leaders and teams across functions like customer support, operations, compliance, and engineering get the guidance they need to build AI knowledge that translates into execution.

Our role-specific AI training is grounded in real retail banking workflows, so your front and back office teams, from customer support and relationship managers to compliance and operations, understand how to use AI as agents rather than just banking chatbots. By seeing how AI enhances their day-to-day work, they’re more likely to adopt it rather than resist it.

Meanwhile, hands-on executive training helps your senior leaders build the strategic clarity needed to understand where AI fits, evaluate which use cases are worth pursuing, and see how competitors are already deploying AI.

This way, they have a clear roadmap for implementation. They’re also better able to rally teams behind AI.

For example, a regional branch of a major global bank needed to improve its executives’ understanding of AI and increase adoption of AI internally.

We designed hands-on executive AI training tailored to their institution, covering AI fundamentals for financial services, their competitive positioning, real BFSI use cases, and practical exercises. The bank’s senior leaders left with a clear understanding of AI’s capabilities and the confidence to champion AI adoption across their organization.

When your teams and leadership understand how to use AI the right way, your existing tools move from supporting isolated tasks to enabling real workflows for significant impact across your operations.

Establish the Data, Governance and Evaluation Frameworks for Compliant and Scalable AI

Without the right data, governance, and evaluation frameworks in place, it’s difficult to move beyond surface-level tasks like Q&A or content generation and support complex retail banking use cases in a secure, reliable way.

With Neurons Lab’s deep AI and financial services expertise, you get a foundation that allows your AI systems to operate across processes like KYC, onboarding, lending, and customer support while remaining compliant with requirements such as AML controls, transaction monitoring, and customer data protection.

Your data is unified and prepared across systems, including customer records, transaction histories, and documents, so agents can reliably retrieve and act on it in real time. This is done within governance frameworks aligned with standards like GDPR and ISO/IEC 27001.

With Neurons Lab, you maintain full control over how AI operates through agent-level guardrails, defining what data can be accessed, what actions can be taken (e.g., updating records or initiating transactions), and under what conditions. This means your customer data stays private, outputs are accurate, and your systems remain compliant.

To ensure governance works in practice, not just on paper, our forward-deployed engineers (FDEs) work directly with your teams to translate policies and compliance rules into agent workflows, embedding decision logic and edge cases into how the system behaves. This ensures outputs are controlled, auditable, and aligned with regulatory requirements from day one.

You also receive structured AI agent evaluation frameworks with testing for accuracy, hallucination monitoring, and validation against expected business outcomes and performance metrics, allowing your teams to continuously assess and improve performance over time through continuous optimization.

With Neurons Lab, you can be confident your AI systems are production-ready, auditable, and aligned with regulatory requirements, with full traceability of how decisions are made.

Build and Scale AI Agents on Your Existing Systems with Expert Support

Setting up existing AI tools to handle multi-step workflows like onboarding and customer support and getting them to work across different systems (e.g., core banking systems and document processing tools) without the right AI development team and expertise is challenging.

Neurons Lab gives you the expert support and delivery model you need to build and scale agentic AI more efficiently across your bank. This means you’ll be able to go beyond mere automation and delegate context-heavy, multi-step tasks to AI—similar to assigning work to a junior team member—while your teams retain ultimate accountability and oversight.

Our forward-deployed experts work alongside your teams to accelerate implementation, turning internal workflows into production-ready agent protocols that integrate directly with your existing technology ecosystem.

With our AI accelerator solution, you also get a faster way to scale custom AI agents organization-wide.

Instead of building from scratch, the accelerator gives you ready-to-use, customizable AI skills, such as document extraction and customer interaction handling, that you can combine to handle retail banking workflows like KYC, personalization, and collections.

And because our accelerator solution works alongside your existing AI tools, rather than replacing them, you move directly to building agents without sacrificing reliability or compliance.

For example, if you combine document analysis and chat capabilities to build a KYC agent for your compliance team, you can reuse those same capabilities to build a loan processing agent or a customer support agent that verifies identity before acting on a request. This allows you to scale artificial intelligence across your various departments in weeks rather than months, while keeping your AI deployment costs low.

How a Commercial Bank Achieved 85% Reduction in Document Processing Time with Agentic AI

A major commercial bank was processing financial documents manually, creating bottlenecks, high operational costs, and compliance risks. The challenge was compounded by documents submitted in multiple languages, including handwritten text, that the bank’s existing systems couldn’t handle.

Neurons Lab built an AI-driven intelligent document processing system that automatically ingests, reads, and extracts key information from financial documents across multiple languages and formats.

It identifies relevant financial details with full traceability and produces structured JSON outputs. The system also automates compliance validation and integrates with the bank’s infrastructure through secure APIs deployed on AWS.

As a result, the bank has seen:

- 85% reduction in manual processing time, freeing teams to focus on higher-value work

- 80% extraction accuracy across multi-language financial documents

- Support for three languages, including English, Russian, and Kazakh, across both printed and handwritten submissions

Choose a Partner That Helps You Get More Value From Your AI for Retail Banking

To see significant operational value from AI, you need systems that can access your data, make decisions, and take action across retail banking workflows in a compliant way.

This requires the right data foundation, governance structures, system architecture, and delivery model to scale AI across the organization. Your teams also need to understand how to use these systems effectively.

The right partnership works with you across all of these areas, from aligning leadership and defining a clear AI roadmap to upskilling your teams and building production-ready agentic systems.

If you’re ready to apply AI across your retail banking workflows with a specialized financial services partner, get in touch with us today.

FAQs

How long does it take to deploy AI Agents for retail banking?

Timelines vary based on how you approach the build. Fully custom solutions often take several months because of the complexity involved, especially when you need to integrate with legacy systems, prepare data, set up governance, and test performance in regulated workflows.

Working with an AI partner specialized in financial services like Neurons Lab that already has a proven system and delivery model can shorten it to weeks.

Which AI use cases deliver the fastest ROI in retail banking?

The fastest ROI comes from high-volume, department-wide use cases that span entire workflows rather than isolated tasks. Examples include customer support that both handles complex requests and takes action, KYC and onboarding workflows that process documents end-to-end, or collections processes that prioritize and manage outreach automatically.

What skills do teams need to successfully use AI in retail banking?

Different teams need different capabilities. Front and back office teams need to understand how to use AI in their day-to-day work, review outputs, and ensure results align with internal controls and compliance requirements.

Domain experts need to translate their knowledge into structured instructions that agents can follow, and help define how edge cases should be handled.

Technical teams need to integrate these agent capabilities into existing systems and manage data access. Together, this creates a setup where you can continuously govern AI and improve AI.